Recent statutory changes under the FY 2026 National Defense Authorization Act revise the applicability thresholds for the Cost Accounting Standards and limit certain post-award contract price adjustments. These updates affect how contractors evaluate fixed-price awards, accounting practice changes, and clause timing, as regulatory implementation is expected within 180 days of enactment.

Read More

Topics:

Accounting System Compliance,

Contracts & Subcontracts Administration,

DCAA Audit Support,

Government Regulations,

Cost Accounting Standards (CAS)

For the last few years, our friends at the Defense Contract Audit Agency (DCAA) have been very helpful by publishing the Contractor Compensation Cap in the December timeframe. This year, I am guessing that the Government shutdown has diverted their attention. To help our clients, we have calculated the 2026 amount of the cap.

Read More

Topics:

Accounting System Compliance,

Proposal Cost Volume Development & Pricing,

Employee & Contractor Compensation,

Incurred Cost Proposal Submission (ICP/ICE),

DCAA Audit Support,

Human Resources,

Government Regulations,

Federal Acquisition Regulation (FAR)

On December 5, 2025, the Department of Justice (DOJ) reported another settlement under the False Claims Act (FCA) related to cybersecurity. Swiss Automation agreed to pay $421,234 to the Government as a result of failing to provide adequate cybersecurity controls for drawings of parts supplied to Department of Defense (DoD) prime contractors. The qui tam suit under the False Claims Act (FCA) was brought forward by a whistleblower, not an Information Technology (IT) employee, but a Quality Control Manager of the company. The whistleblower received $65,291.

Read More

Topics:

Contracts & Subcontracts Administration,

DFARS Business Systems,

Contractor Purchasing System Review (CPSR),

Government Regulations,

Federal Acquisition Regulation (FAR),

Material Management & Accounting System (MMAS),

Cybersecurity,

Commercial Determination

EO 14173 revoked EO 11246 Equal Employment Opportunity, which required covered federal contractors to practice affirmative action, develop written Affirmative Action Plans (AAPs) and implement compliant programs directed towards equal opportunities for women and minorities. This major change left contractors with a choice: set aside all efforts previously made toward compliance with EO 11246, or continue with employment analytics under a framework acceptable under EO 14173. In this article, we explain why we encourage you to consider the continuation of these efforts.

Read More

Topics:

Contracts & Subcontracts Administration,

Human Resources,

Government Regulations,

Office of Federal Contract Compliance Programs,

Service Contract Act

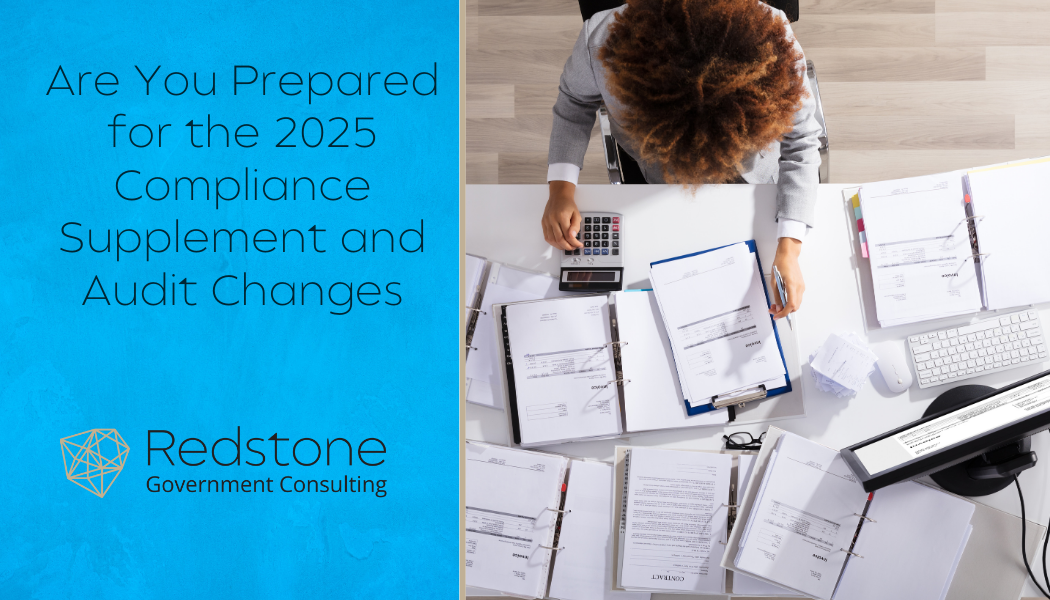

On November 26, 2025, the Office of Management and Budget (OMB) issued the 2025 Compliance Supplement. The Supplement outlines the compliance requirements to assist auditors in understanding the Federal program’s objectives, procedures and requirements when performing a Single audit for fiscal years beginning after June 30, 2024. The Compliance Supplement is normally issued in the spring of each year; however, OMB delayed its issuance to incorporate significant updates to 2 CFR 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, in October 2024. In order to assist auditors with the different requirements, Part 3 Compliance Requirements of the Supplement was divided into two Parts for audit testing as follows:

- Part 3.1 for awards subject to 2 CFR 200 prior to October 2024 and

- Part 3.2 for awards after October 1, 2024

Read More

Topics:

Accounting System Compliance,

DFARS Business Systems,

DCAA Audit Support,

Contractor Purchasing System Review (CPSR),

Government Regulations,

Grants & Cooperative Agreements (2 CFR 200)

The Department of Defense (DoD) issued a final rule on September 10, 2025, amending the Defense Federal Acquisition Regulation Supplement (DFARS) to incorporate the requirements of the Cybersecurity Maturity Model Certification (CMMC) for FAR-based contracts and subcontracts, effective November 10, 2025.

Read More

Topics:

Small Business Compliance,

Contracts & Subcontracts Administration,

DFARS Business Systems,

Government Regulations,

Federal Acquisition Regulation (FAR),

Cybersecurity,

Grants & Cooperative Agreements (2 CFR 200)

The January 2025 EO 14173, Ending Illegal Discrimination and Restoring Merit-Based Opportunity, triggered mixed emotions amongst HR professionals in the GovCon community – shock, disappointment, and celebration, to name a few. While all might not agree with the requirements of EO 14173, most likely agree that it has caused a great deal of confusion and uncertainty about what is expected, or, more importantly, what is no longer allowed of government contractors. In a previous article released shortly after the EO was signed, we outlined the crux of the EO and overarching implications. As time has passed and more information has come to light, including Attorney General Bondi’s July 2025 memo for federal agencies, we are gleaning additional insights to share.

Read More

Topics:

Small Business Compliance,

Contracts & Subcontracts Administration,

Human Resources,

Government Regulations,

Office of Federal Contract Compliance Programs,

Service Contract Act

%20Apply%20to%20Fixed%20Price%20Contracts%20and%20Subcontracts.png)

%202026.png)

%20Requirements%20Apply%20to%20Grants.png)