This is the second blog in a three-part series on progress payments. This blog addresses Line 5, Contract Price and Line 11, Total eligible costs on the SF1443 Contractor’s Request for Progress Payment Form.

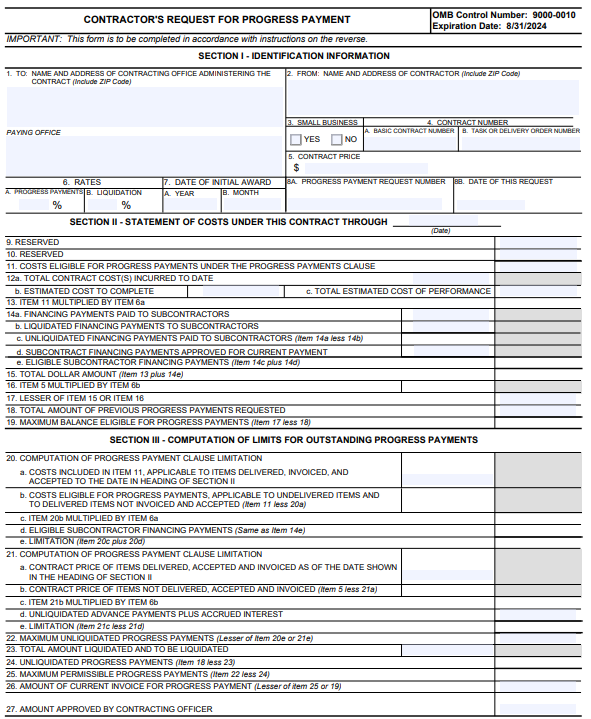

Example SF1443 – Contractor’s Request for Progress Payment

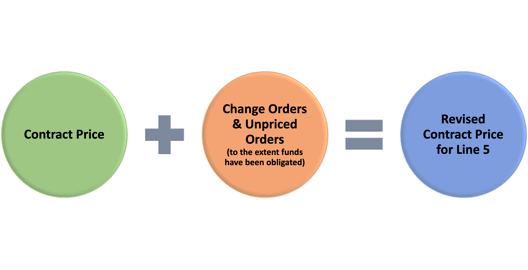

What Amount Goes into Line 5, Contract Price on the SF1443?

The contract price is the following:

The contract price does not include any CLINS in the contract that are cost reimbursable. The contract price will align with the Estimate at Completion (EAC) which is the Estimate to Complete plus the incurred cost to date on Line 12, provided there is no potential loss requiring adjustment. ETC’s will be addressed in the third blog of this three-part series on Progress Payments.

The contract price does not include any CLINS in the contract that are cost reimbursable. The contract price will align with the Estimate at Completion (EAC) which is the Estimate to Complete plus the incurred cost to date on Line 12, provided there is no potential loss requiring adjustment. ETC’s will be addressed in the third blog of this three-part series on Progress Payments.

So, What are “Eligible” Costs in Line 11 of the SF1443?

Eligible costs are total costs incurred under the contract whether or not actually paid. However, FAR 52.232-16(a)(2) has a limitation that the costs cannot be included in the progress payment request unless the amount due to be paid to subcontractors meets two criteria:

- In accordance with terms and conditions of subcontract or invoice and,

- Ordinarily within 30 days of submission of the contractor’s progress payment request to the Government.

The “amount due to be paid to subcontractor” above refers to vendor, supplier, or subcontract invoices where items or services are received, and payment is made. Line 11 does not include subcontract costs where the contractor has set up financing with the subcontractor such as commercial payments, performance-based payments, or progress payments. Financing costs between the contractor and subcontractor are reported on Line 14 of the SF1443.

So, what happens if my supplier’s invoice has payment terms of 120 days, and the material was received and booked to the general ledger/job cost. Can the cost be submitted on Line 11? Probably not. There is an “and” in the clause, therefore both requirements have to be met in order to include the costs on Line 11. A contractor would need to pay the subcontract invoice earlier than 120 days (e.g., generally within 30 days of the progress payment request to the government).

When DCAA performs payment reviews, they select material/subcontract invoices and verify that the costs included in the progress payment request have been paid or will be paid in 30 days of the request to the government. This includes reviewing the accounts payable aging reports to verify that the dates on the invoices and payment dates match the aging report and verify that checks are not being held.

Indirect Costs and Cost of Money Included in Line 11

Indirect costs reflect the indirect rates applied to the appropriate direct costs whether it is overhead rates, fringe rates or G&A rates and are included in Line 11. DCMA/DCAA will ensure that the rates are based on the approved provisional billing rates which exclude unallowable costs. If a contractor does not have approved billing rates, the government will establish rates by making adjustments to the prior year actuals, adjusting for unallowables and changed conditions. Prior year costs need to be calculated using the most up to date rates – year end or final indirect rates.

Cost of money can be included in Line 11 as long as it is allowable under FAR 31.205-10 as an incurred cost. Cost of money can only be billed as an allowable cost if it is proposed on the contract and the FAR 52.215-16, Facilities Capital Cost of Money, clause is included in the contract.

What Costs are Included in Line 11 if the contract has First Article Approval?

If the contract has a first article contract line item, then the only costs that can be submitted on Line 11 of the SF1443 are the costs associated with the first article until it is approved. Contractors should make sure a separate project number is set up to account for first article costs. Any costs associated with materials or production in advance of obtaining first article approval are at the risk of the contractor unless the Contracting Officer approves a line item before first article approval (e.g., long lead material). This is addressed in FAR 52.209-3(g) First Article Approval – Contractor Testing or FAR 52.209-4(h) First Article Approval – Government Testing.

Contractors should ensure the correct contract price is used in Line 4 of the SF1443. More importantly contractors should review the accounts payable aging report and make sure any material costs that are not going to be paid, generally within 30 days of the progress payment request to the government, are excluded from Line 11 of the SF1443.

Redstone GCI is available to assist contractors and subcontractors in their preparation of progress payment requests, review eligible costs for progress payments and assist in developing provisional billing rates to bill indirect costs. Redstone GCI assists contractors throughout the U.S. and internationally with understanding the Government’s expectations and requirements related to compliance with Government contracting terms and conditions.

Lynne is a Director with Redstone Government Consulting, Inc. providing government contract consulting services to our clients primarily related to Commercial Item Determinations and support, Cost Accounting Standards, DFARS Business System Audits, Proposals, and Incurred Cost. Prior to joining Redstone Government Consulting, Lynne served in several capacities with DCAA and DCMA for over 35 years. Professional Experience Lynne began her career working with DCAA in the Honeywell Resident Office, Clearwater, FL in 1984. Lynne’s experience included various positions which involved conducting or reviewing forward proposals or rate audits, financial capability audits, progress payments, accounting and estimating systems, cost accounting standards, claims and disclosure statement reviews. She is an expert in FAR, DFARS, CAS and testified as an expert witness. Lynne assisted in drafting the commercial item guidance for DCAA Headquarters. Lynne was assigned as a Regional Technical Specialist where she provided guidance to 20 field offices on highly complex or technical issues relative to forward pricing, financial capability or progress payment issues. As an Assistant for Quality, she was involved in reviewing and ensuring audit reports were in compliance with policy and GAGAS as well as made NASBA certified presentations to the staff including but not limited to billing reviews, CAS, unallowable cost and progress payments. To enhance her experience in government contracting, Lynne accepted a position with DCMA in 2015 as part of the newly organized DCMA Cadre of Experts in the Commercial Item Group. This included performing reviews of prime contractor’s assertions and/or commercial item determinations as well as performing price analyses. Lynne was a project lead and later became a lead analyst where she engaged with the buying commands on requests and reviewed price analysis reviews performed by a team of 5 analysts. She also assisted the DCMA CPSR team relative to commercial items and co-instructed the Commercial Item Training presented to DCMA. Education Lynne earned a Bachelor of Science Degree in Accounting from the University of Central Florida. Certifications State of Florida Certified Public Accountant State of Alabama Certified Public Accountant Defense Acquisition Workforce Improvement Act (DAWIA) Level III- Auditing DAWIA Level III – Contracting

Lynne is a Director with Redstone Government Consulting, Inc. providing government contract consulting services to our clients primarily related to Commercial Item Determinations and support, Cost Accounting Standards, DFARS Business System Audits, Proposals, and Incurred Cost. Prior to joining Redstone Government Consulting, Lynne served in several capacities with DCAA and DCMA for over 35 years. Professional Experience Lynne began her career working with DCAA in the Honeywell Resident Office, Clearwater, FL in 1984. Lynne’s experience included various positions which involved conducting or reviewing forward proposals or rate audits, financial capability audits, progress payments, accounting and estimating systems, cost accounting standards, claims and disclosure statement reviews. She is an expert in FAR, DFARS, CAS and testified as an expert witness. Lynne assisted in drafting the commercial item guidance for DCAA Headquarters. Lynne was assigned as a Regional Technical Specialist where she provided guidance to 20 field offices on highly complex or technical issues relative to forward pricing, financial capability or progress payment issues. As an Assistant for Quality, she was involved in reviewing and ensuring audit reports were in compliance with policy and GAGAS as well as made NASBA certified presentations to the staff including but not limited to billing reviews, CAS, unallowable cost and progress payments. To enhance her experience in government contracting, Lynne accepted a position with DCMA in 2015 as part of the newly organized DCMA Cadre of Experts in the Commercial Item Group. This included performing reviews of prime contractor’s assertions and/or commercial item determinations as well as performing price analyses. Lynne was a project lead and later became a lead analyst where she engaged with the buying commands on requests and reviewed price analysis reviews performed by a team of 5 analysts. She also assisted the DCMA CPSR team relative to commercial items and co-instructed the Commercial Item Training presented to DCMA. Education Lynne earned a Bachelor of Science Degree in Accounting from the University of Central Florida. Certifications State of Florida Certified Public Accountant State of Alabama Certified Public Accountant Defense Acquisition Workforce Improvement Act (DAWIA) Level III- Auditing DAWIA Level III – Contracting