How much do you know about DCAA and its oversight of your incurred cost proposals (ICP) and indirect cost rates? Would it help to understand what is done and why? Knowing what initiates a DCAA audit of an incurred cost proposal and maintaining a good system of internal controls can potentially keep you from audit.

Prior to 2020, DCAA was faced with an incurred cost audit backlog that it just seemed not to be able to get out from under. There were stories about DCAA wanting to audit incurred cost submissions that were not even supported by the current company’s IT platform and some auditors wanting to audit records 7-plus years old. Since DCAA seemed unable to get itself from under its backlog, it got help from outside of DCAA. The DoD 809 Panel and its “Professional Practice Guide – Audits and Oversight of Defense Contractor Costs and Internal Controls” revamped DCAA’s audit process and made it more risk-based. This risk-based process was not just based quantitatively on dollars but also qualitatively on contractor prior audit findings and its processes to comply with contracting regulations.

Who Gets Audited and Why?

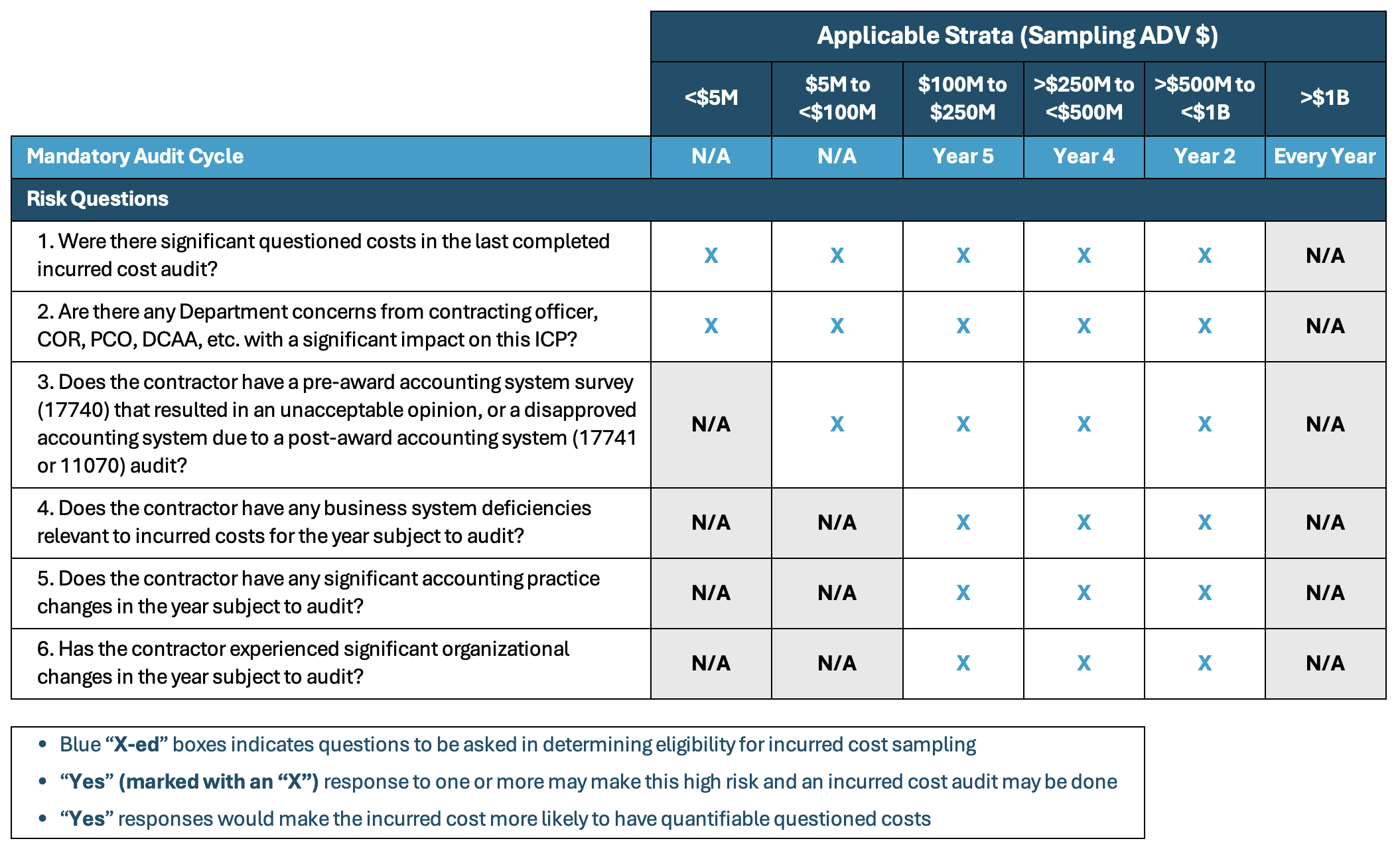

This guide and its risk-based approach were adopted by DCAA, starting with contractor submissions received after 2020. This risk-based approach would take into consideration the ICP subject matter (related to contractor flexibly priced contracts dollars) as well as additional questions over internal controls and prior ICP questioned costs and audit deficiencies. This is shown in the table below.

DCAA Incurred Cost Risk Assessment Table

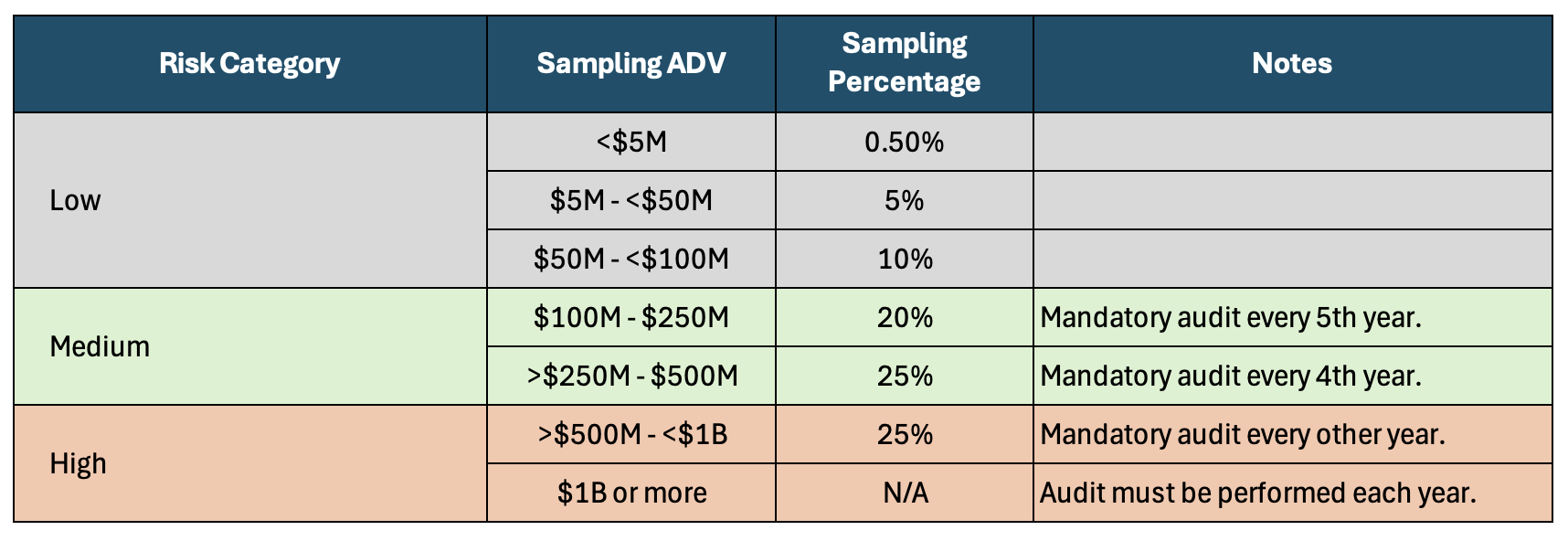

The result from this table is used to establish three levels of strata risk: low, medium, and high. Each contractor's ICP is evaluated for its sampling eligibility. If something indicates high risk (as shown in questions #3 through #6 above), then the contractor’s ICP may be deemed to be ineligible for sampling, and an audit of their ICP would be conducted. If eligible for sampling and there is no greater risk associated (as shown in questions #3 through #6), then a sampling of contractors’ ICPs would be performed through DCAA Headquarters sampling process using the sampling percentages shown below.

Percentages of Selection for Incurred Cost Audit Through the Sampling Selection

(From DCAA Policy and Procedures for Risk-Based Sampling of Incurred Cost Proposals Version 2.0)

From this, you can see that if you are in the low-risk category, there is an advantage to being eligible for ICP sampling. That means that a contractor needs to be actively involved in maintaining their adequate accounting system as well as adequate screening of unallowable costs. Also, you can conclude that staying in, perhaps, the low-risk category has its advantage in that you have a chance of selection of no more than 10%.

Looking at the trend since this was adopted, you can see that in 2023, for example, incurred cost audits only amounted to 583 of the total of incurred cost audit reports and low-risk memos, or merely 18% were audited, and 82% were low-risk (no audit) memos for use in administering indirect rates applied to flexibly priced contracts. The information below was taken from DCAA’s Report to Congress for its fiscal years 2020 through 2023.

DCAA Secret to Efficiency – Low Risk Sampling of Incurred Cost

Best Practices

- Have policies and procedures that address high-risk cost areas (e.g., compensation, consultants, travel, etc.).

- Train your employees on FAR/CAS requirements including upper-level management, accounting, compliance, recognizing unallowable costs in FAR Part 31.2, etc.

- Monitor your controls.

- Walk your approving official who signs the certification through the ICP.

- Monitor your billing rates, adjust when necessary, and close out contracts as soon as possible.

- Use the ICP adequacy checklist to identify any shortcomings or deficiencies prior to submission to the government.

With this knowledge, you know what to expect and what you can control. In summary, the goal should be to remain sampling eligible, and your reward is a lower chance of being selected for audit.

Get It Right Before You Submit with ICP and FAR Part 31 Support

Redstone GCI supports government contractors in navigating the complexities of incurred cost submissions and DCAA oversight. Our team offers focused training for your staff on allowable costs, unallowable cost screening, and the nuances of FAR Part 31. We routinely review incurred cost proposals (ICPs) prior to submission, helping contractors identify and resolve issues before they attract government scrutiny. With years of experience addressing complex FAR Part 31 cost principles, Redstone GCI helps government contractors build accurate incurred cost proposals and maintain compliance throughout the audit process. Whether you need help preparing your ICP or responding to a DCAA audit, our team is here to support you at every step.

David (Dave) Fix is a Director with Redstone Government Consulting, Inc. He provides Government Contract Consulting services to our Government contractors primarily related to compliance with Federal Acquisition Regulations and Cost Accounting Standards, equitable adjustment claims, and business systems. Prior to joining Redstone Government Consulting, Dave served in a number of capacities with DCAA for over 35 years. Upon his retirement, Dave was a Regional Audit Manager with DCAA. Dave began his DCAA career in 1986 as an auditor-trainee with the General Electric Suboffice in Pittsfield, Massachusetts. He progressed from auditor to DCAA management ranks serving in DCAA offices in Upstate New York, Columbus, Ohio and Greensboro, North Carolina in audits of major and non-major contractors. Dave served DCAA in three overseas tours, all as Branch Manager, in Kuwait/Iraq (2007), Afghanistan (2010-2012) and Kuwait (2014). Dave was promoted to Regional Special Programs Manager (RSPM) in 2015 before ultimately becoming a Regional Audit Manager (RAM) in October 2019. While a RSPM, Dave worked with DCAA’s other three RSPMs with updating the Agency-wide audit planning process including assigning priorities and determining funded/unfunded audits that is currently being used by DCAA. While a RAM, Dave had overall management responsibility for audits performed by approximately 140 employees including one of DCAA’s largest shipyards. During his career, he served as guest instructor at DCAA’s Defense Contract Audit Institute (DCAI) bringing field perspective to “Advance Auditing Issues” and “Supervisors’ Course” as well as served as a DCAI adjunct instructor over DCAA auditors’ initial two-week training course prior to his retirement. Dave served 36 years in the Air Force Reserve/Air National Guard in both enlisted and officer positions retiring at the rank of Lieutenant Colonel. His last duty station was Air Force Reserve Command (AFRC) Headquarters, Robins Air Force Base, Inspector General Office serving as the Chief, Contracting Inspections leading inspections of AFRC’s 10 contracting offices as well as assisting in inspections of AFRC finance offices. Dave currently specializes in preparing clients for more complex DCAA audits, providing advice on FAR cost principles and contracts regulatory provisions and in assisting clients in anticipating and addressing audit.

David (Dave) Fix is a Director with Redstone Government Consulting, Inc. He provides Government Contract Consulting services to our Government contractors primarily related to compliance with Federal Acquisition Regulations and Cost Accounting Standards, equitable adjustment claims, and business systems. Prior to joining Redstone Government Consulting, Dave served in a number of capacities with DCAA for over 35 years. Upon his retirement, Dave was a Regional Audit Manager with DCAA. Dave began his DCAA career in 1986 as an auditor-trainee with the General Electric Suboffice in Pittsfield, Massachusetts. He progressed from auditor to DCAA management ranks serving in DCAA offices in Upstate New York, Columbus, Ohio and Greensboro, North Carolina in audits of major and non-major contractors. Dave served DCAA in three overseas tours, all as Branch Manager, in Kuwait/Iraq (2007), Afghanistan (2010-2012) and Kuwait (2014). Dave was promoted to Regional Special Programs Manager (RSPM) in 2015 before ultimately becoming a Regional Audit Manager (RAM) in October 2019. While a RSPM, Dave worked with DCAA’s other three RSPMs with updating the Agency-wide audit planning process including assigning priorities and determining funded/unfunded audits that is currently being used by DCAA. While a RAM, Dave had overall management responsibility for audits performed by approximately 140 employees including one of DCAA’s largest shipyards. During his career, he served as guest instructor at DCAA’s Defense Contract Audit Institute (DCAI) bringing field perspective to “Advance Auditing Issues” and “Supervisors’ Course” as well as served as a DCAI adjunct instructor over DCAA auditors’ initial two-week training course prior to his retirement. Dave served 36 years in the Air Force Reserve/Air National Guard in both enlisted and officer positions retiring at the rank of Lieutenant Colonel. His last duty station was Air Force Reserve Command (AFRC) Headquarters, Robins Air Force Base, Inspector General Office serving as the Chief, Contracting Inspections leading inspections of AFRC’s 10 contracting offices as well as assisting in inspections of AFRC finance offices. Dave currently specializes in preparing clients for more complex DCAA audits, providing advice on FAR cost principles and contracts regulatory provisions and in assisting clients in anticipating and addressing audit.