So, you have been notified by the Defense Contract Audit Agency (DCAA) that they plan on performing an incurred cost audit. What comes next? How is this audit being performed? You are probably not going to get this background from your DCAA auditor. This article will go over the process that will be applied to take a little of the “mystery” away.

DCAA’s incurred cost oversight was changed in the last few years through the issuance of the DoD Professional Practice Guide (PPG) – Audits and Oversight of Defense Contractor Costs and Internal Controls. The PPG recommends adoption of commercial based risk and materiality and a consistent audit approach whether being audited by an independent public accountant (IPA) or by government auditors, such as DCAA. Initially, DCAA will do its typical requests for information of your incurred cost claim. DCAA will also request an entrance conference date and a “walkthrough” of your submission. However, unless you had a DCAA incurred cost audit in the last few years, you may not be aware of how the audit is performed.

Identification of Subject Matter Costs Sorted by Cost Elements

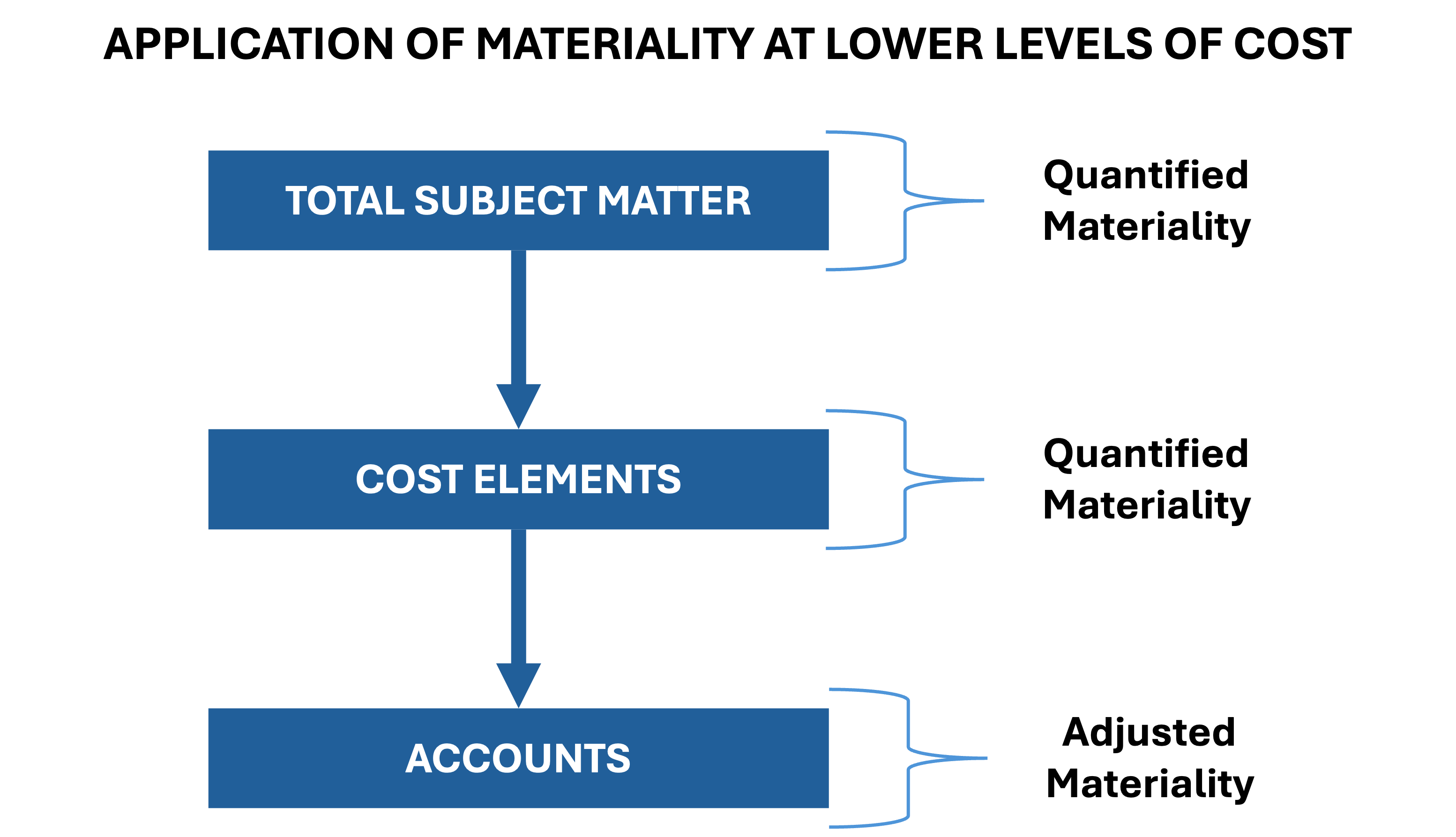

It starts at what is under audit through the identification of the subject matter costs. The subject matter costs is roughly your costs on flexibly priced (for example, cost-type contracts) and billed time & material contracts, less any unclaimed costs. The resulting cost is what will be audited under the incurred costs audit. Then, the auditor will identify the subject matters costs by cost elements such as direct materials, direct labor, other direct costs, subcontracts, and indirect expenses such as overhead and general and administrative expenses applicable to the subject matter costs. Next will be identification of materiality.

Quantified Materiality Applied to Subject Matter Costs

DCAA and its auditors used to struggle with materiality and “how much matters” in its incurred cost audits. For example, what was material varied from auditor to auditor. The PPG provided guidance and addresses “how much matters” through a consistent quantified materiality. The quantified materiality is calculated using an algebraic formula, Quantified Materiality Formula, to derive the materiality percentages applied to the subject matter costs under audit. The intent of the quantified materiality is to create a consistent threshold for establishing materiality. See below how the PPG shows this.

|

Subject Matter Cost |

$100K |

$1M |

$10M |

$100M |

$500M |

$1B |

> $1B |

|

Materiality Amount |

$5,000 |

$28,117 |

$158,686 |

$889,140 |

$2,973,018 |

$5,000,000 |

Varies |

|

Materiality Percentage |

5% |

2.81% |

1.58% |

0.89% |

0.59% |

0.50% |

0.50% |

As you can see, range varies with the dollar strata, from 5% at the lower dollar such as $100 thousand ($5 thousand) to 0.5% at $1 billion ($5 million) of subject matter costs. Next, this formula is applied to the subject matter costs deriving the quantified materiality to the cost elements and then down to the account level through adjusted materiality. To visualize this, see below (taken from PPG).

Example

Using an example of a $11,325,911 of subject matter costs would be calculated as shown below (taken from a DCAA course implementing PPG).

|

Quantified Materiality Calculation (Audit Subject Matter from $1 to $1,000,000,000) |

|

|

Total Subject Matter of Audit |

$11,325,911 |

|

Quantitative Materiality Formula |

= 5000*((Subject Matter of Audit/100000)^.75) |

|

Quantitative Materiality Threshold |

$173,590 |

So, $173,590 would be considered material due to the cost elements (taken from a DCAA course implementing PPG) as shown below.

|

Cost Element |

Amount |

Quantified |

Exceed |

|

Direct Labor |

$ 5,184,819 |

$ 173,590 |

YES |

|

Direct Travel |

136,153 |

$ 173,590 |

NO |

|

Direct Material |

2,285,178 |

$ 173,590 |

YES |

|

ODC |

94,026 |

$ 173,590 |

NO |

|

Subcontracts |

931,963 |

$ 173,590 |

YES |

|

Overhead |

1,354,342 |

$ 173,590 |

YES |

|

G&A |

1,339,430 |

$ 173,590 |

YES |

|

|

$ 11,325,911 |

|

|

A YES in the table above means the cost element is significant and should be further evaluated at the account level, but it does mean the entire amount will be tested. From this, you can see that direct travel and ODC are under the quantified materiality threshold. Cost elements, such as these two, may be tested if there are certain risks that combined could be material. However, this is more of the exception than the rule. So, after the cost elements for further review have been identified, the next step is to identify the significant accounts for review through the Adjusted Materiality.

Adjusted Materiality Applied to Accounts

A significant account is identified by adjusted materiality, this is less than quantified materiality, to identify significant accounts for audit evaluation. Adjusted materiality is used at a more discrete level in the books and records and is applied to accounts that make up the cost elements. For purposes of selecting accounts for audit testing, adjusted materiality can be stated as 20 percent to 80 percent of quantified materiality (see below). The adjusted materiality also brings in a qualitative component of risk with the contractor under audit. Generally, the auditor will reduce quantified materiality by 20 percent. An example below is an application of the stated adjusted materiality (taken from a DCAA course implementing PPG).

|

Examples |

Percent |

Quantified |

Amount Adjusted |

|

#1 |

20% |

$ 173,590 |

$ 138,872 |

|

#2 |

50% |

$ 173,590 |

$ 86,795 |

|

#3 |

80% |

$ 173,590 |

$ 34,718 |

- Example 1 – 20% Reduction in Quantified Materiality [Best for contractor – testing larger accounts and less accounts tested] - The cost element and accounts do not have historical material misstatements.

- Example 2 – 50% Reduction in Quantified Materiality - The cost element and multiple accounts have a history of material misstatements, and the contracting officer has concerns regarding the cost element that increase the sensitivity and importance.

- Example 3 – 80% Reduction in Quantified Materiality [Worst for contractor – testing smaller accounts and more accounts tested] - There is a history of material misstatements in multiple accounts; the contractor is unwilling to correct prior-year material misstatements in subsequent proposals; and the contracting officer has significant concerns. In summary, in this example, more audit testing is warranted due to higher risk of finding more of “what matters.”

Other Considerations

- PPG also provides guidance on how to calculate adjusted materiality for indirect costs where the government’s participation is less than 100%. Under this situation, indirect costs for audit evaluation are prorated and will increase the adjusted materiality depending upon the government participation level.

- Generally, if the cost element is material and the accounts are less than adjusted materiality, then similar accounts could be combined for audit.

- Additionally, audits must be completed within one year of the date of receipt of the qualified (adequate) incurred cost submission.

As you can see, the PPG directed consistency among IPAs or a government auditors and materiality determination under audit. Knowing how you are being audited takes some of the mystery away and assists you in a successful audit.

Redstone GCI can assist you in several key areas. We provide assistance in preparing and determining the adequacy of your incurred cost submission. Our services also include staff training on government contracting and improving your accounting system for government contract compliance. Additionally, we can augment your team for audit support, ensuring your organization is well-prepared and compliant.

David (Dave) Fix is a Director with Redstone Government Consulting, Inc. He provides Government Contract Consulting services to our Government contractors primarily related to compliance with Federal Acquisition Regulations and Cost Accounting Standards, equitable adjustment claims, and business systems. Prior to joining Redstone Government Consulting, Dave served in a number of capacities with DCAA for over 35 years. Upon his retirement, Dave was a Regional Audit Manager with DCAA. Dave began his DCAA career in 1986 as an auditor-trainee with the General Electric Suboffice in Pittsfield, Massachusetts. He progressed from auditor to DCAA management ranks serving in DCAA offices in Upstate New York, Columbus, Ohio and Greensboro, North Carolina in audits of major and non-major contractors. Dave served DCAA in three overseas tours, all as Branch Manager, in Kuwait/Iraq (2007), Afghanistan (2010-2012) and Kuwait (2014). Dave was promoted to Regional Special Programs Manager (RSPM) in 2015 before ultimately becoming a Regional Audit Manager (RAM) in October 2019. While a RSPM, Dave worked with DCAA’s other three RSPMs with updating the Agency-wide audit planning process including assigning priorities and determining funded/unfunded audits that is currently being used by DCAA. While a RAM, Dave had overall management responsibility for audits performed by approximately 140 employees including one of DCAA’s largest shipyards. During his career, he served as guest instructor at DCAA’s Defense Contract Audit Institute (DCAI) bringing field perspective to “Advance Auditing Issues” and “Supervisors’ Course” as well as served as a DCAI adjunct instructor over DCAA auditors’ initial two-week training course prior to his retirement. Dave served 36 years in the Air Force Reserve/Air National Guard in both enlisted and officer positions retiring at the rank of Lieutenant Colonel. His last duty station was Air Force Reserve Command (AFRC) Headquarters, Robins Air Force Base, Inspector General Office serving as the Chief, Contracting Inspections leading inspections of AFRC’s 10 contracting offices as well as assisting in inspections of AFRC finance offices. Dave currently specializes in preparing clients for more complex DCAA audits, providing advice on FAR cost principles and contracts regulatory provisions and in assisting clients in anticipating and addressing audit.

David (Dave) Fix is a Director with Redstone Government Consulting, Inc. He provides Government Contract Consulting services to our Government contractors primarily related to compliance with Federal Acquisition Regulations and Cost Accounting Standards, equitable adjustment claims, and business systems. Prior to joining Redstone Government Consulting, Dave served in a number of capacities with DCAA for over 35 years. Upon his retirement, Dave was a Regional Audit Manager with DCAA. Dave began his DCAA career in 1986 as an auditor-trainee with the General Electric Suboffice in Pittsfield, Massachusetts. He progressed from auditor to DCAA management ranks serving in DCAA offices in Upstate New York, Columbus, Ohio and Greensboro, North Carolina in audits of major and non-major contractors. Dave served DCAA in three overseas tours, all as Branch Manager, in Kuwait/Iraq (2007), Afghanistan (2010-2012) and Kuwait (2014). Dave was promoted to Regional Special Programs Manager (RSPM) in 2015 before ultimately becoming a Regional Audit Manager (RAM) in October 2019. While a RSPM, Dave worked with DCAA’s other three RSPMs with updating the Agency-wide audit planning process including assigning priorities and determining funded/unfunded audits that is currently being used by DCAA. While a RAM, Dave had overall management responsibility for audits performed by approximately 140 employees including one of DCAA’s largest shipyards. During his career, he served as guest instructor at DCAA’s Defense Contract Audit Institute (DCAI) bringing field perspective to “Advance Auditing Issues” and “Supervisors’ Course” as well as served as a DCAI adjunct instructor over DCAA auditors’ initial two-week training course prior to his retirement. Dave served 36 years in the Air Force Reserve/Air National Guard in both enlisted and officer positions retiring at the rank of Lieutenant Colonel. His last duty station was Air Force Reserve Command (AFRC) Headquarters, Robins Air Force Base, Inspector General Office serving as the Chief, Contracting Inspections leading inspections of AFRC’s 10 contracting offices as well as assisting in inspections of AFRC finance offices. Dave currently specializes in preparing clients for more complex DCAA audits, providing advice on FAR cost principles and contracts regulatory provisions and in assisting clients in anticipating and addressing audit.