The Defense Contract Audit Agency (DCAA) issued a memorandum to its leadership – and ultimately its auditors in the field – addressing a revision to its audit guidance related to the audit of contractor cost impact calculations for unilateral cost accounting practice changes (23-PAC-009(R) Revised Audit Guidance on the Cost Impact Calculation for a Unilateral Cost Accounting Practice Change – dated October 3, 2023). Well, it is about time.

Interestingly – The “Why did we revise the guidance?” section states the “change in audit guidance [is] to reflect certain Armed Services Board of Contract Appeals (ASBCA) decisions and their application to the range of unilateral CAP change scenarios.” If I am not mistaken, the ASBCA case in question was the May 7, 2015, Raytheon case (ASBCA Cases 57801, 57803, 58068). Ok, maybe for DCAA, that is a fast turn...some eight years after the fact. Or maybe they were hoping that no one would read the case.

The Good News

The guidance states that “the fourth step in FAR 30.604(h)(iv) to calculate the increased cost to the Government in the aggregate, is more than just a mathematical calculation.” If they had simply stopped there – but oh no. The guidance also instructed auditors that “DCAA will no longer recommend settlement alternatives” because that is the job of the deciding official – DCAA, not trying to do someone else’s job – that could be a first.

The Bad News

DCAA still does not want to fully consider the second part of 9903.201-4(a)(2)(a)(5), which states:

In no case shall the Government recover costs greater than the increased cost to the Government, in the aggregate, on the relevant contracts subject to the price adjustment…

First, DCAA makes an assumption that the costs from the Cost Accounting Practice (CAP) change that shifted from the affected fixed price contracts/subcontracts to the affected flexibly priced contracts/subcontracts may not be the “same” cost. The guidance provides that “the auditor should confirm whether the unilateral CAP change shifted the same costs from the fixed price to the flexibly priced contracts/subcontracts group.” Emphasis added. In the DCAA Cost Impact Audit Program (19500), a single sentence was added to assist the auditor, stating: “The auditor should consider whether or not the increased or (decreased) costs to the Government are the result of a reallocation/shifting of the same costs among contract/subcontract types when determining the increased cost in the aggregate.” I am concerned that this will lead to the auditor simply issuing a data request to the contractor saying prove the costs are the same, or they will have to issue a qualified opinion or even a disclaimed opinion. This is hard to believe – allocations are like squeezing a balloon; the air in the balloon has not changed, it just ends up in a different space. Changing an allocation does not change the cost being allocated, it simply reallocates the SAME cost.

Second, the remaining scenarios developed by DCAA all require the auditor to take the largest increased cost amount, whether it is on the fixed price contracts/subcontracts or the flexibly priced (i.e., cost type) contracts/subcontracts. This does not fit with the CAS requirement for the Government to recover the increased cost in the aggregate and no more. The Board has found that this amount should be based on comparing what the Government would have paid without the change to what it will pay with the change. DCAA’s own scenarios point out my concern.

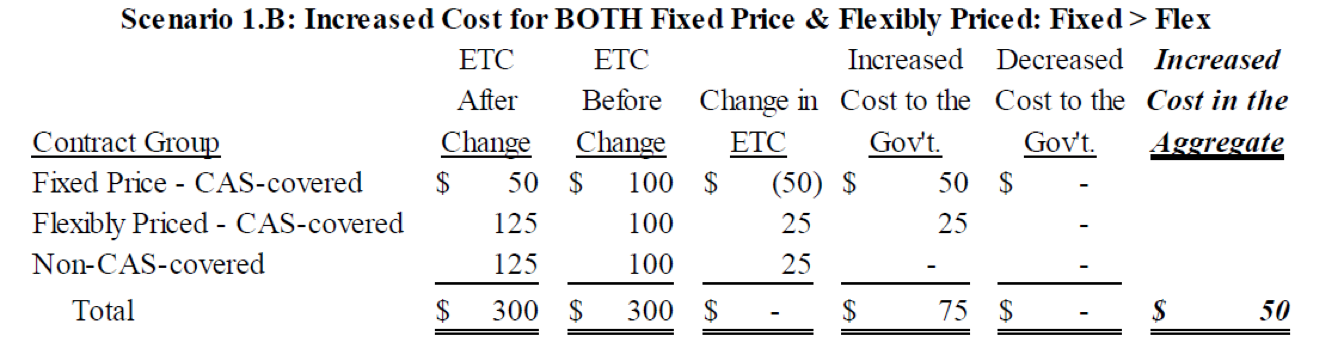

In Scenario 1.B (see above), before the change, the Government is going to pay $100 on fixed-price CAS-covered contracts and $100 on flexibly priced CAS-covered contracts for a total of $200. After the change, the Government would end up paying $100 on fixed-covered contracts if no adjustment to the contract price was made and $125 on flexibly priced CAS-covered contracts for a total of $225 – for an increased cost in the aggregate of only $25, not the $50 to be reported by DCAA. As DCAA’s own guidance states: “Special consideration is needed when a unilateral CAP change results in increased cost to both the flexibly priced and/or fixed price contract/subcontract groups to ensure the estimated increased cost to the Government “in the aggregate” is equitable.” Determining the total amount, the Government would have paid before the change and comparing it to the total amount the Government will pay after the change represents the equitable amount of increased cost in the aggregate.

I do not believe DCAA’s position of taking the biggest number is reasonable guidance and is likely to lead to additional differences between DCAA audits and contractor calculations – and, yes, more litigation in the future.

Our Takeaway

When faced with developing a cost impact (general dollar magnitude or detail contract by contract cost impact), focus on the impact of what the Government was going to pay vs. what they are likely to pay after the change.

Redstone GCI assists contractors throughout the U.S. and internationally with understanding the Government’s expectations and supporting contractors with the development of cost impacts. We would be happy to be part of your team.

John is a Director with Redstone Government Consulting, Inc. providing government contract consulting services to our clients primarily related to the DFARS business systems, CAS Disclosure Statements, and DCAA/DCMA compliance preparation, advisory, and defense. Prior to joining Redstone Government Consulting, John served in a number of capacities with DCAA/DCMA for more than 30 years. Upon his retirement, he was based in Texas as an SES-level Corporate Audit Director for DCAA, managing a staff of 300 auditors at one of the largest DOD programs. Professional Experience John began his career in the late 80s working in the Clearwater, FL audit office and over the next three decades he progressed through a number of positions within both DCAA and DCMA with career highlights as DCAA Program Manager at Ft. Belvoir, Chief of Technical Programs Division, Deputy Assistant Director-Policy, Director of the DCMA Cost and Pricing Center, the SES-level Lockheed Martin Corporate Audit Director, and Director of Integrity and Quality Assurance. John’s three decades of experience in performing and leading DCAA auditors and DCMA reviewers provides a wealth of expertise to our clients. John’s role, not only in the performance of audits, but also in the development of audit policy affords him unique insights into the defense of audit findings and the linkage of audit program steps to the underlying regulatory framework. He is an expert in FAR, DFARS, and other agency acquisition regulation, as well as a subject matter expert in the Cost Accounting Standards having reviewed and provided audit feedback on many of the largest and most complex cost accounting practices during his tenure with the DCAA. John’s tenure with DCAA and DCMA came at a critical time during each agency’s history where a number of changes were occurring such as the response to the ICS backlog, development of audit approaches to the DFARS Business Systems and implementation of new audit initiatives as a result of Congressional oversight through the NDAA process. John’s leadership at the DCMA Cost & Pricing center saw oversight of all major DOD pricing actions, leadership of should cost review teams, the Commercial Pricing group and many other areas of strategic value to our clients. His involvement in these and other Agency initiatives is of great value to our clients due to his in depth understanding of DCAA and DCMA’s internal policy directives. Education John holds a Master of Business Administration and a B.A. in Accounting from the University of South Florida. Certifications Certified Information Systems Auditor State of Alabama Certified Public Accountant

John is a Director with Redstone Government Consulting, Inc. providing government contract consulting services to our clients primarily related to the DFARS business systems, CAS Disclosure Statements, and DCAA/DCMA compliance preparation, advisory, and defense. Prior to joining Redstone Government Consulting, John served in a number of capacities with DCAA/DCMA for more than 30 years. Upon his retirement, he was based in Texas as an SES-level Corporate Audit Director for DCAA, managing a staff of 300 auditors at one of the largest DOD programs. Professional Experience John began his career in the late 80s working in the Clearwater, FL audit office and over the next three decades he progressed through a number of positions within both DCAA and DCMA with career highlights as DCAA Program Manager at Ft. Belvoir, Chief of Technical Programs Division, Deputy Assistant Director-Policy, Director of the DCMA Cost and Pricing Center, the SES-level Lockheed Martin Corporate Audit Director, and Director of Integrity and Quality Assurance. John’s three decades of experience in performing and leading DCAA auditors and DCMA reviewers provides a wealth of expertise to our clients. John’s role, not only in the performance of audits, but also in the development of audit policy affords him unique insights into the defense of audit findings and the linkage of audit program steps to the underlying regulatory framework. He is an expert in FAR, DFARS, and other agency acquisition regulation, as well as a subject matter expert in the Cost Accounting Standards having reviewed and provided audit feedback on many of the largest and most complex cost accounting practices during his tenure with the DCAA. John’s tenure with DCAA and DCMA came at a critical time during each agency’s history where a number of changes were occurring such as the response to the ICS backlog, development of audit approaches to the DFARS Business Systems and implementation of new audit initiatives as a result of Congressional oversight through the NDAA process. John’s leadership at the DCMA Cost & Pricing center saw oversight of all major DOD pricing actions, leadership of should cost review teams, the Commercial Pricing group and many other areas of strategic value to our clients. His involvement in these and other Agency initiatives is of great value to our clients due to his in depth understanding of DCAA and DCMA’s internal policy directives. Education John holds a Master of Business Administration and a B.A. in Accounting from the University of South Florida. Certifications Certified Information Systems Auditor State of Alabama Certified Public Accountant