In today’s budgets constrained environment U.S. Government contracting officers are seeking every opportunity to obtain discounted or reduced prices for services and materials, and as a tax payer that should make us all happy. However, for those of us who work in the government contracting industry the sight of LPTA solicitations, and enhanced scrutiny of proposals does make work life more challenging. One of the areas that we see challenged by contracting officers either during the proposal process or after award is the application of G&A on direct travel associated with the contract. This might be a solicitation provision, a Government expectation for contractor concessions during negotiations or a Government interpretation after contract award.

As a contractor balancing cost recovery with appeasing the customer, your options vary with pushing back to the contracting officer. Five points to consider in this process are as follows:

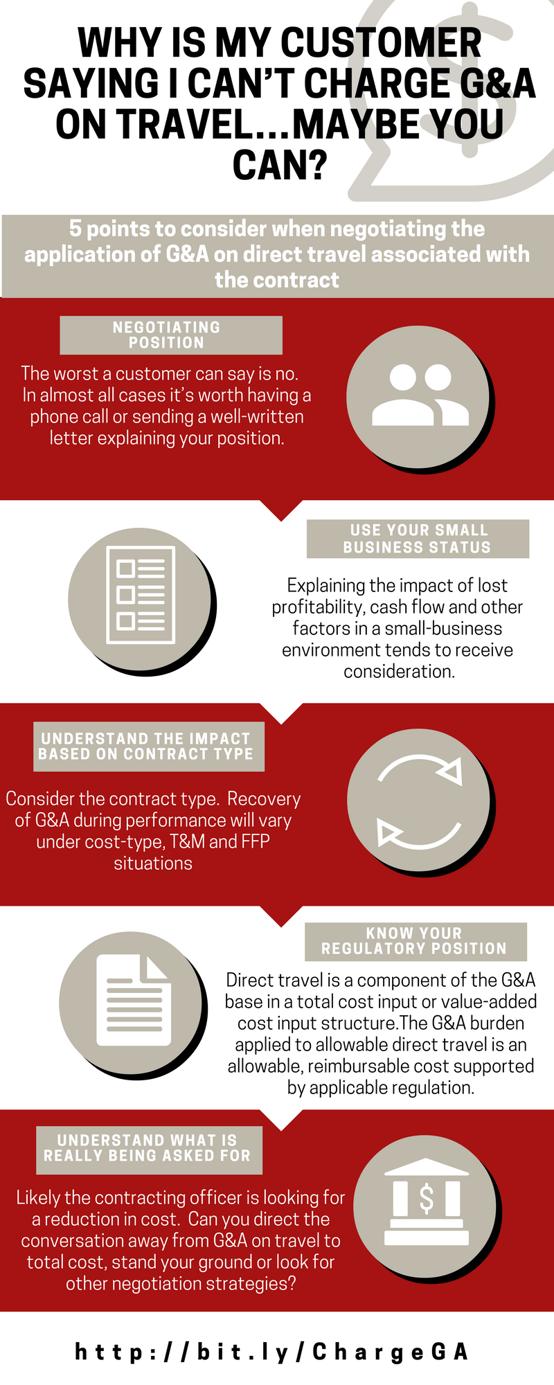

- Obviously the most important consideration is your negotiating position. How critical is the contract and the customer relationship. I am a firm believer that the worst a customer can say is no, so in almost all cases it’s worth having a phone call or sending a well written letter explaining your position (more on that below). However, depending on the situation and the impact to contract profitability the best course of action may be simply to agree to disagree (i.e. do not make the concession).

- Use your small business status as leverage if applicable. The simple fact of the matter is that in almost all cases direct travel is a component of the G&A base, which means that G&A is will be allocated to direct travel, it just might not be billable. In the case where it is allowable, but not billable there is a direct reduction of profit on the contract. Explaining this fact and the impact of lost profitability, cash flow and other factors in a small-business environment tends to receive some consideration from reasonable contracting officers.

- Understand the impact by contract type.

- Cost-type – dollar for dollar loss of revenue and direct reduction in profitability assuming G&A on direct travel is not recoverable. Assuming a hypothetical 10% G&A rate and $100K in direct travel we would be looking at a 10 cent loss for every dollar of direct travel billed. If the contract is heavily labor driven and you have the profitability on that aspect to withstand this loss on travel you may be OK, but be cognizant of smaller contracts where the ratio of travel to other expenses is higher. Your ability to make up the difference through efficiencies (other cost reductions) does not exist, since those efficiencies are passed on directly to the customer.

- Time-and-Material – As a hybrid contract type with fixed labor rates and cost reimbursable material the actual loss as a result of not being able to bill G&A on travel is much the same as a cost-type contract. A key difference is that the loss of 10 cents per dollar of direct travel would be the same as the cost-type example, but the loss could be mitigated through the fixed labor rates as well as profit. If a contractor can underrun costs on its fixed “T” labor rates, there is at least the potential to offset unbillable G&A against higher profits on the fixed component of the T&M contract.

- FFP – under a FFP contract pricing is fixed at the outset of the contract, so really we are primarily concerned with the ability to propose G&A on direct travel to make sure it is included in the fixed price. Fixing travel costs, particularly airfare is always a challenge due to the volatility in airline and travel prices in general. The key here is that if you know G&A cannot be proposed, then ensure your travel estimates are realistic and err on the high-side of any proposed travel costs to insulate yourself not only from fluctuations, but also from the known loss on the G&A applied to direct travel under the FFP contract.

- Know your regulatory position. For CAS-covered contractors there are three acceptable G&A structures, with Total Cost Input (TCI) and Value-Added Cost Input (VACI) being by far the most common. Under each of these scenarios, assuming you do not have a travel administration overhead (service center), direct travel is a component of the G&A base. By inclusion of direct travel cost in the G&A base, the resulting allocation is a component of the total cost of procuring travel for a contract. Many contracting officers mistakenly assume that G&A on travel is additional fee or profit, which is false. The cost to procure, administer, manage and seek approval, as well as the all too often changes in travel requirements are all housed within the G&A pool and performed (typically) by G&A staff members. The cost of travel is not simply the cost of the airfare and per diems. FAR 31.202 and 203 require consistency in the classification of direct and indirect cost, and for contractors where direct travel is consistently a component of the G&A base removing direct travel from the G&A base is not an option, unless the circumstances or purpose surrounding the incurrence of travel is different from other direct travel incurred for similar purposes or in like circumstances (highly unlikely). Finally, absolutely nothing within the FAR or CAS prohibits the recovery of the administrative (G&A) expenses associated with the incurrence of direct travel a fact which was reinforced when FAR 52.232-7 (T&M Contract) was changed in 2007. If a contracting officer is seeking to disallow G&A on travel and the contract does not explicitly state that this cost is unallowable, the regulations (included in the contract) clearly support allocating and billing G&A on direct travel.

- Understand what the contracting officer is asking for by not allowing G&A on travel. As noted above there is nothing within regulation which prohibits the recovery of G&A on travel, so what is the contracting officer really getting at? Well, quite simply, a reduction in cost. If the CO is after a reduction why not seek to meet them in the middle with a reduced G&A recovery on travel or perhaps a slightly lower fixed fee or profit. Leave your cost accounting intact, and reduce the overall price to the Government through other means.

In summary, G&A on travel is an allowable, ordinary and necessary cost associated with travel in support of contracts and seeking to recover this cost is perfectly acceptable. Knowing your contracting officer’s true motivation is key to unraveling this point of negotiation, along with understanding your negotiating position and using any other leverage you may have (small-business) to seek an amicable resolution to these issues. For contractors who are seeing very frequent push back on this topic, development of an alternate rate strategy to exclude direct travel from the G&A base may be a consideration as well, which is something we have assisted several contractors with doing over the past few years. In addition, there have been several recent cases which are beyond the scope of this article that may be of interest in debating this topic with your customer. We’d be interested in your feedback on this topic and any insights you may have for dealing with this all too frequent issue, and as always don’t hesitate to reach out to us if we can assist with this topic or any of your other government compliance challenges.