“My DCAA auditor is telling me I’m now subject to CAS. What does that mean? What do I do?”

We at Redstone get questions like this almost every day. Usually we then obtain as much information as we can to determine why DCAA has made this claim and advise our clients accordingly.

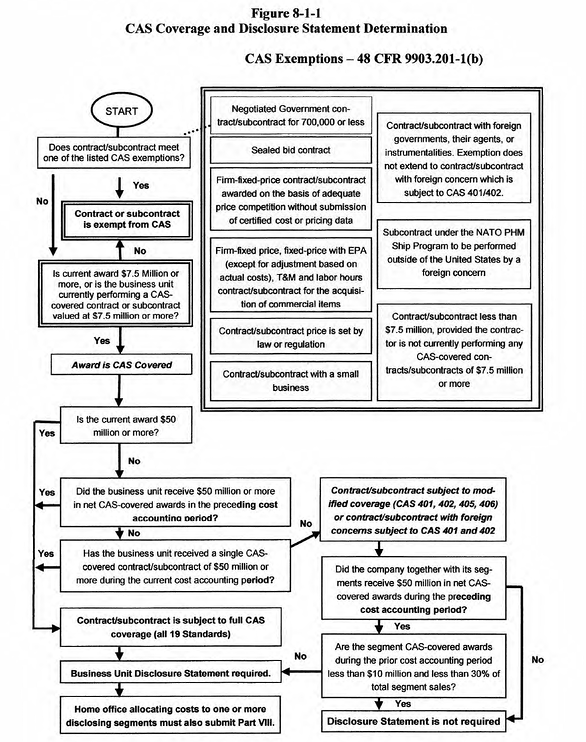

Let’s look at what most likely prompted the DCAA auditor’s assertion. Based on the DCAA auditor’s knowledge of the contractor and its awards or a request for audit from a contracting officer ready to award a potentially CAS covered contract the auditor will make a preliminary determination of the type of CAS coverage, if any. This determination would be based on the requirements of 48 CFR Subpart 9903 which requires certain contractors and subcontractors to comply with Cost Accounting Standards (CAS) and to disclose them in writing and to consistently follow their cost accounting practices. However, if the auditor does not recall the criteria off the top of their head then they will refer to Figure 8-1-1 (see flowchart attached) set forth in chapter eight of the DCAA Contract Audit Manual (CAM). After the auditor determines that the client does not meet one of the several CAS exemptions then the auditor is asked “Is current award $7.5 Million or more, or is the business unit currently performing a CAS covered contract or subcontract valued at $7.5 million or more?” If the answer is NO then the contract or subcontract is exempted from CAS. However, if the answer is YES then the award is CAS covered.

The auditor will then make the following determinations:(i) If the current award is $50 million or more or if less than $50 million but the client receive $50 million or more in net CAS covered awards in the preceding cost accounting period or the client received a single CAS covered contract/subcontract of $50 million or more during the current cost accounting period the contract or subcontract is subject to full CAS coverage or all of the 19 standards and the client must file a CAS disclosure statement, or (ii) If the answer to all of the questions in (i) is NO then the contract/subcontract is subject to modified CAS coverage or CAS 401, 402, 405, and 406 or a contract/subcontract with foreign concerns are subject to CAS 401 and 402 only. There are nuances to determining when a contract/subcontract subject to modified CAS coverage requires CAS disclosure statement submission and must be addressed also.

Needless to say the downside to becoming CAS covered is the probable increase in paperwork but the silver lining we always like to point out is that the company is growing with the increases to contract awards. Regardless of whether a company is Full or Modified CAS covered or not CAS covered at all, Redstone can assist with the proper determination and submission of necessary documentation. Furthermore, we provide training via seminars and webinars addressing all aspects of CAS. Please explore our website, www.redstonegci.com, for more information.